Summary

- Alpha’s exploration work has provided more information on the value of its properties.

- Its landholdings are in very close proximity to those of three major lithium producers.

- Alpha has been the subject of takeover talk in the past.

Alpha Lithium Corporation (OTCPK:APHLF) is in the very early stages of developing its Argentinian claims. It has yet to fully explore its properties and has not even released a Preliminary Economic Assessment (“PEA”), making any estimate of the project’s timeline and final costs nothing but a guess. But that’s not what interests me about the company, as I believe there is a good chance that Alpha may never reach commercial production. A look at the location of Alpha’s land holdings and who its neighbors are, makes me think that there is a high probability the company will be bought out before ever reaching production.

In media interviews earlier this year, Brad Nichol, the CEO of Alpha Lithium, briefly discussed in vague terms how Alpha had received “expressions of interest” from “several companies”. But that was a while ago and a good amount of time has since passed, and obviously, a deal was never struck. Also, judging by the 40% pullback in the company’s stock price over the last couple of months, it’s clear that any excitement about a potential deal has largely fizzled out.

However, I think that discarding the possibility of any eventual takeover or buyout may be premature. While this is pure speculation on my part, I believe the exploration work that Alpha has done so far may lead one or more of the major lithium producers that also own property in the same Salar to put in a bid for the junior miner. At such point, investors would receive a nice premium for their shares.

Company Backgrounder

Alpha Lithium is a pre-production lithium producer with landholdings in the Argentinean part of the Lithium Triangle. Its primary holdings are a 28k hectare block in the Tolillar Salar as well as a series of tracts in the neighboring Hombre Muerto Salar that total just over 5k hectares.

Over recent years, the company has been carrying out exploratory work at Tolillar and more recently at Hombre Muerto. Much of this was very preliminary work that consisted of Vertical Electrical Sounding (“VES”) studies geared towards assessing the size and limits of the aquifers from which the brine will eventually be extracted.

At Tolillar the company has managed to drill 15 exploration wells, but the results for these have not been great, with the average grade coming in at 270 mg/L and magnesium content at 6.0 Mg:Li. The good news, however, is that a preliminary resource estimate for Tolillar put LCE at over 2.1Mt Indicated and just under 1.2Mt Inferred, and that only accounts for 32% of the property as the balance has not yet been explored. Also of note, is the brine’s potassium content which averaged between 2,201 and 2,315 mg/L which translates to ~7.4Mt KCI Equivalent of Indicated resource and ~4.8Mt KCI Equivalent of Inferred. That is not insignificant given the jump in potassium chloride prices this year.

As far as the low lithium grades go, Alpha plans to employ proprietary Direct Lithium Extraction (“DLE”) technology, which it claims has a much higher recovery rate than the typical 40%-50% recoveries achieved through conventional evaporation ponds. In these efforts, Alpha has worked with Lilac Solutions and Beyond Lithium LLC, two DLE providers that have worked with numerous other brine producers. Alpha has built a pilot plant which yielded 12,000 mg/L of lithium concentrate utilizing its DLE tech, which can be used to produce high-grade LiOH and Li2CO3. But as is the case with almost all DLE processes, except for Livent Corporation (LTHM), it remains to be seen whether these results can be used at full-scale production.

The company also recently announced very ambitious plans to build a conversion facility capable of producing up to 40ktpa of high-purity carbonate. Detailed engineering work on the pilot plant has begun and the company hopes to eventually issue a PEA report for the facility.

And while the conversion plant, along with the previously-mentioned proprietary DLE technology, are great and will one day probably help generate substantial revenue, they’re not what interest me about Alpha Lithium and its $100m market cap. Because for some reason, when I look at this company and its land holdings, the only thing I can think about are the three most important rules of real estate.

Location, Location, Location

Investor Presentation

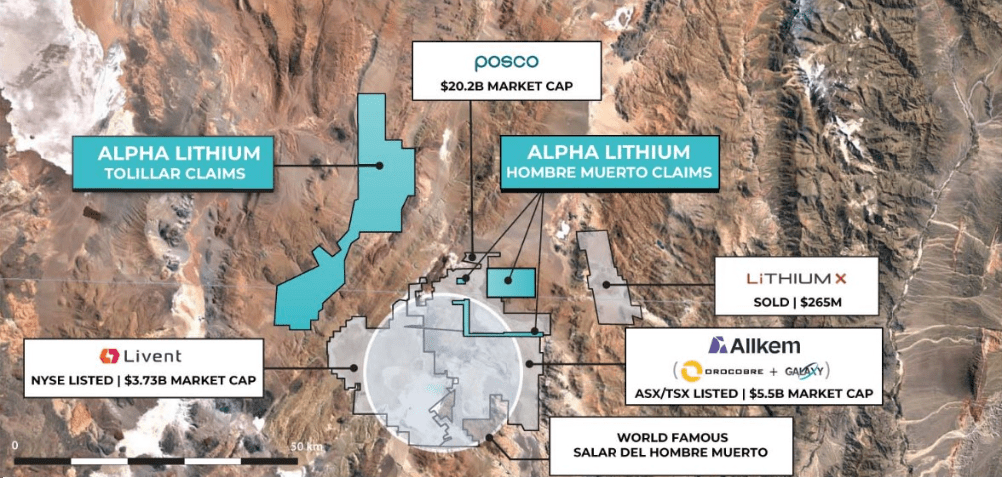

It’s very hard not to notice who Alpha’s neighbors are. In fact, if this particular corner of the Lithium Triangle were a fish tank, Alpha would be a minnow surrounded by three giant bull sharks.

POSCO Holdings Inc. (PKX) is a South Korean steelmaker with interests in several other industries including battery materials. Earlier this year, it announced plans to invest $4 billion in its Hombre Muerto property as it eventually plans to build out brine extraction facilities as well as hydroxide plants capable of producing 100ktpa of the chemical. It is currently doing advanced exploration work and expects to begin some commercial production by the end of 2023.

In the initial press release announcing the project, POSCO listed one of its goals as “increasing cathode material business competitiveness by securing a large amount of lithium”. The company also states that “POSCO Group plans to become one of the top three global lithium production companies by 2030”. If you look at the map above, you’ll notice that part of Alpha’s Hombre Muerto claim lies right in the middle of POSCO’s property; forming a small island right in the middle of a property that will eventually have $4 billion of assets on it.

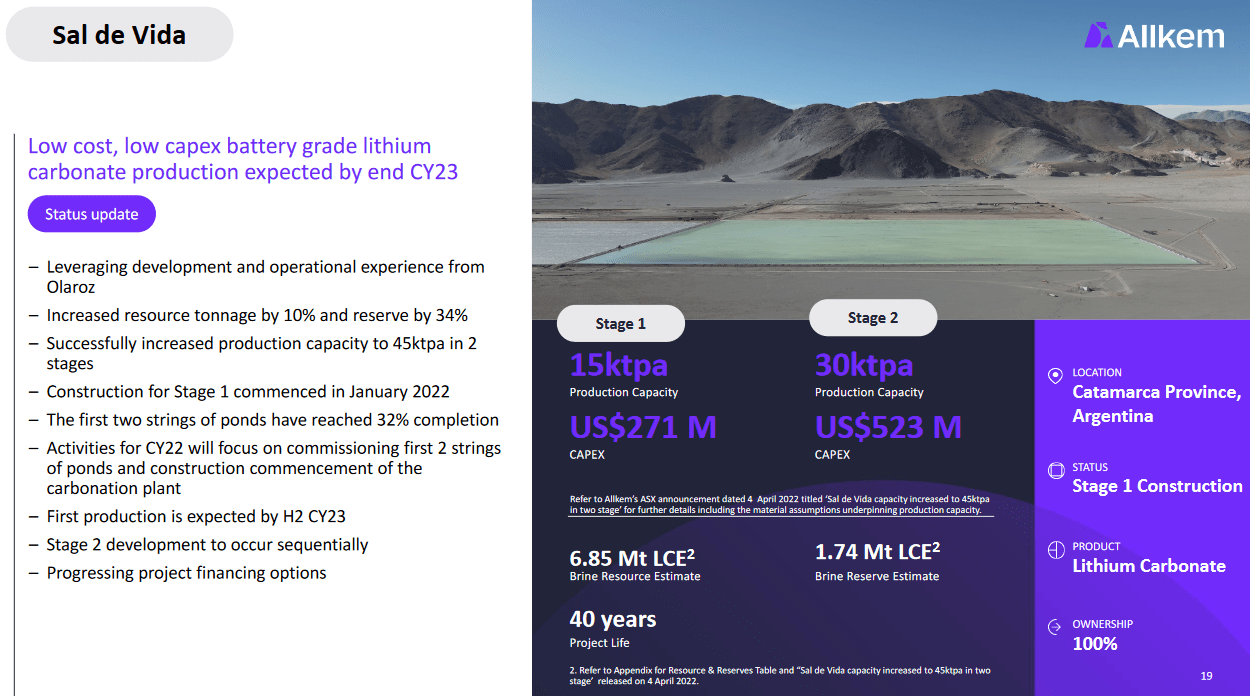

Right next door is Allkem Limited (OTCPK:OROCF), a company about which I have written on two occasions here and here. Allkem’s management, who have set a goal of maintaining a 10% share of the global lithium market, are currently building their Sal de Vida project in the Hombre Muerto Salar. The property is still in development and expects to see first production in the second half of 2023, it will eventually produce 45ktpa of carbonate.

Allkem Investor Presentation

Allkem is serious about maintaining that 10% global market share and is ambitiously pursuing multiple midstream and upstream projects. So, it wouldn’t come as a surprise if they decided to grow their reserves through the purchase of some Alpha assets.

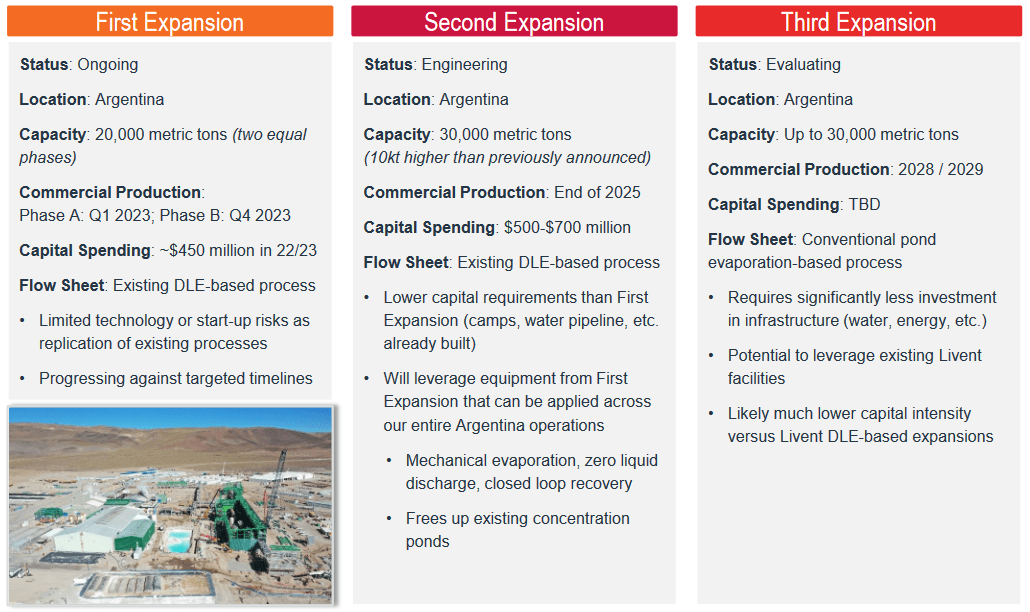

Third on the list is Livent, of which I have previously written about here. Its Hombre Muerto property is a mere 10 kilometres away from Alpha’s Tolillar claim, and the company has been extracting lithium from this property for years. As I discussed in my article, Livent is currently one of the most sought-after lithium producers on the planet. General Motors Company (GM) had to pay it almost $200 million upfront to secure a hydroxide offtake agreement that won’t see first deliveries until 2025. And like all the other lithium majors, Livent is currently building up its midstream capacity. Its plans include the addition of 80ktpa of carbonate conversion at its Argentinian operations over the coming years.

Livent Investor Presentation

Those are impressive amounts to be sure, but they don’t even factor in conversion capacity that’s also being added at Livent’s Bessemer City and Chinese operations. One can imagine a scenario whereby Livent needs to secure more feedstock, and begins looking around the neighborhood in order to find it.

Takeaway

Given each of these companies’ ambitious growth strategies, along with the fact that those strategies have a strong focus on adding midstream capacity, leads one to believe that they will probably want to grow their reserves. This would make a lot of sense as it would give the conversion facilities on which they are spending hundreds of millions, or even billions, much longer productive lives. And Alpha’s properties are perfectly located to do just that.

The fact that there are many potential suitors is also a nice plus as it could drive the price higher. As many readers are probably aware, there have been other transactions for nearby properties, but many of those occurred when lithium prices were much lower. However, if we look to the purchase of Rincon Mining by Rio Tinto Group (RIO) for $825 million earlier this year, we can get a sense of Alpha’s value.

The average grade of Rincon’s lithium was 250 mg/L, which is very close to that of Alpha. Granted, Rincon’s resource size came in at 7.9Mt (M&I&I) which is 2.5x larger than Alpha’s 3.277Mt (I&I), but using these numbers does allow us to put a $330 million price estimate on Alpha. That would certainly be a nice premium to Alpha’s current share price and would surely please investors.

Risks

The risk to this thesis, of course, is that no deal is ever consummated. In that case, shareholders would have to wait until Alpha’s management got production up and running, and during that time would be subject to the ups and downs of lithium prices and the lithium market.