Summary

- Arena Minerals is being acquired. Early buyers of Arena are selling shares and trying to find new speculative homes in the lithium space.

- Alpha Lithium is a small (yet intriguing) lithium stock with a healthy treasury and compelling properties.

- A license was granted to drill the Hombre Muerto property, a very famous Argentinian high-lithium grade basin that is home to very large companies like Livent and POSCO.

- In these wretched market conditions, someone might be accumulating Alpha Lithium stock.

- Those seeking alpha should consider Alpha Lithium as a speculative bet.

BrianAJackson

What is seeking “alpha” and I’m not referring to this web site but what is the concept of seeking an alpha return from an investment prospective? It is simple. Can you beat the market benchmarks? Per Investopedia:

| “Alpha is the return on an investment that is not a result of a general movement in the greater market. As such, an alpha of zero would indicate that the portfolio or fund is tracking perfectly with the benchmark index and that the manager has not added or lost any additional value compared to the broad market.” |

I might argue that when you seek alpha you incur additional risk and that is acceptable. Hence if we want to beat the market averages and produce large gains we must seek some degree of risk. Yet, we must do our homework to place the odds of success in our favor. When seeking alpha one needs to look at lithium and when one looks at lithium one must evaluate some of the smaller riskier companies like Alpha Lithium (OTCPK:APHLF).

Before we get into this article, I want the reader to take note that we are noticing consolidation in the lithium industry. Let’s dedicate a moment of silence for companies below that have been acquired and realize that this is the beginning of the grand consolidation. We will take in a broad overview of acquisitions, recent funding of major projects that impact lithium, and lastly, review Alpha Lithium. Will they be acquired or go to production?

Lithium Consolidation

Below we see company acquisitions in the lithium sector. Many partial acquisitions of projects exist, but to shorten the list we will look only at total company or project purchases. In order of capital spent:

- Ganfeng buys Pozuelos and Pastos Grandes from Lithea for $962 million.

- Rio Tinto (RIO) buys Rincon Mining for $825 million.

- China Zijin Mining (OTCPK:ZIJMF) buys out Neo Lithium for $737 million.

- Wesfarmers (OTCPK:WFAFY) buys Kidman Resources for $534 million.

- China Huayou buys an African mine for $422 million.

- Lithium Americas (LAC) bought out Millennial Lithium for $400 million.

- Lithium Americas is acquiring Arena Minerals (OTCQX:AMRZF) – $227 million.

- China Sinomine Resources Group buys Bikita Minerals – $192 million.

- Tianqi Lithium (Australia) to acquire Essential Metals – $99.4 millionUSD.

- Arizona Lithium (OTCQB:AZLAF) buys Prairie Lithium – $70.6 million.

- Lithium Power International (OTCPK:LTHHF) buys Mineral Salar Blanco – $41 million.

Are you seeing the trend yet? But wait, why so many lithium acquisitions? Could it be because hundreds of billions are flowing into lithium and the associated infrastructure?

Why The Lithium Consolidation?

Frankly, mines take a very long time to go from initial discovery to pulling valuable pay dirt out of the ground. Factor in state and government permitting and it could potentially take 10 to 15 years’ (depending on the project and jurisdiction). Hence, it can be logical to simply pay money to save years of time, if not a decade. However, that is the case with most mining companies. So why the rush to buy lithium? Simple: Demand and geopolitics.

Lithium Demand and Geopolitics

“He who controls the spice controls the universe” – Dune

As I have pointed out (repeatedly) demand for lithium is growing. Supply will increase. Tradingeconomics.com says that Australia projects a 32% global increase in supply in 2023. Lithium Americas is set to bring its South American project “Cauchari-Olaroz” online in the first half of 2023 to the tune of 40,000 tpa. Sigma Lithium (SGML) is talking about a spring-summer launch. These mines coming online could potentially ease price increases, but demand is still obscene and only growing. We may see lithium prices fluctuate but remember, all of the lithium projects NPV (net present value) via various studies factored lithium being in a range of $9,500 to roughly $12,500 dollars. Hence when you see a project with an NVP of $1 billion realize this was conducted at a much lower lithium price.

Hundreds of Billions of Demand

Following the money, you will note hundreds of billions flowing into lithium investments and the associated support infrastructure. Ponder a few and the impact it has. Note: Some of these are not total values; those will be higher. I’ve tried to keep all links from 2022 and those above $1 billion. Otherwise, this list would be very long indeed.

Volkswagen $180 billion.

Ford (F) $50 billion.

Mercedes-Benz $44 billion.

Tesla to build a Gigafactory in Mexico.

GM $7 billion (for just Michigan).

BlueOval SK (a joint venture between SK On and Ford) began to construct two new battery plants in Glendale, Kentucky, US for $6.46 billion.

$4.9 billion in EV upgrades for Ontario per Stellantis & LG Energy Solution.

$3.5 billion via Redwood Materials for a SC plant.

$2.9 billion via California for EV.

$2.36 billion in a Michigan battery component plant via Goition.

$1.6 billion per the Canadian gov.

$1.5 billion for Ottawa and Ontario per Umicore.

$1.4+ billion over five years for Ontario per Honda.

$1 billion in Mexico via GM.

$717 million for Tesla to expand Austin Gigafactory.

Lastly, Tesla is cutting the price of cars in the U.S. and Ford is expanding production of the F-150 Lightning.

Lithium Pricing – Some Thoughts

Lithium prices are trending down. We must at least consider the possibility they drop more. Prices coming down is not a bad thing. The impact on miners that are a few years away from production is lower since they are not near production. Producing or near-term producers could be impacted more as lithium prices stabilize.

Furthermore, lower prices encourage carmakers to keep opening additional lithium-based car factories and this trickles down to battery/cathode makers and ultimately to the lithium miners.

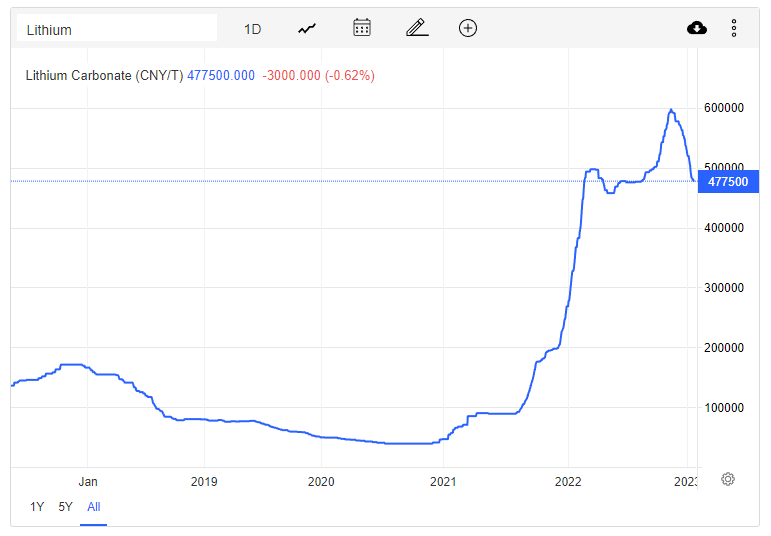

Most PFS (pre-feasibility study) calculations typically use $9,500 to $12,000 per tonne of lithium. Converting the current spot price for lithium carbonate at 477,500 Chinese Yuan to USD (1 Yuan = $0.15) = A current spot market value of $70,688 USD for a tonne of lithium carbonate. Note: Recent contract prices per SQM were about $56,000 a tonne vs spot price. Spot is always higher but has far less sales.

Lithium Prices in Yuan (Tradingeconomics)

Lithium Sensationalism!

Think of spot as what you pay if you are in a jam. The point is, be mentally prepared to see sensational doom and gloom articles pop up about lithium if prices do head down. Yet, remember the NPV (net present value) used in the PFS/DFS studies were calculated using much lower numbers as explained above. Hence, lithium companies are undervalued in relation to the NPV the studies used.

Geopolitics Is Fueling the Sea Change In Energy

Geopolitics also come into play. Frankly, no EV producing company (much less a nation) want to be held hostage to a power that controls a critical element. Hence, forward-planning companies and nations are rushing to secure supply. China has been busy at this for years, but Canada and the U.S. appear to have woken from a deep slumber and are now pledging massive financial support to secure critical elements. The sea change of EV adoption is becoming reality and that brings us to acquisitions. Who yearns to become the next target?

Alpha Lithium Is A Possible Acquisition Target

Alpha Lithium is a lithium exploration company with a market cap of $152 million USD as of January 18, 2023.

I last wrote on Alpha Lithium on Feb 2022 and maybe it is time to give the company some consideration to see if the story has changed. This might allow us to evaluate if we need to simply hold what we have or should we expand our holdings in this stock.

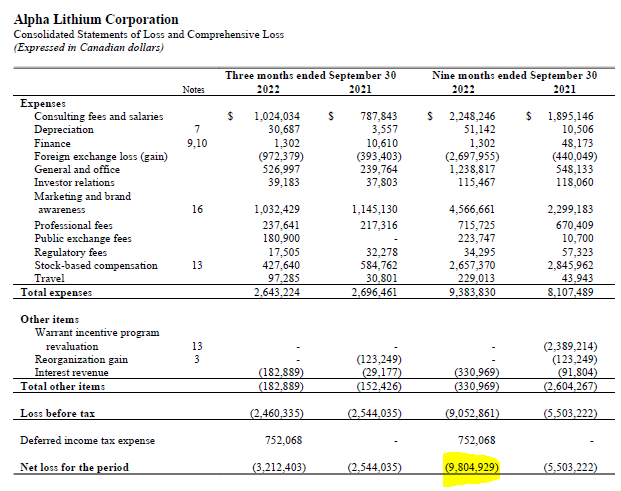

First, we must see if the company is worth our hard-earned dollars by looking at the numbers as a general health check. Glancing at the treasury, we see for the nine months ending Sept 30, 2022, Alpha Lithium had $33.2 million CDN dollars in the bank and accounts receivable at $1.4 million CDN vs Total Liabilities of almost $8 million CDN. The burn rate was $9.8 million for the nine months. That is good enough for now.

Alpha Lithium Finances (Alpha Lithium) |

Alpha Lithium Warrants

Warrants that are utilized equal money the company is paid once they are exercised. It is that simple. Looking at the IR slide deck, we see Alpha has some warrants that are close to price that could be converted at Canadian prices for ticker (ALLI.V) which is trading at $1.21 CDN as of 1/18/2023.

Alpha Lithium Warrants (Alpha Lithium)

We can assume the tranche from 2022 has been executed, thus paying Alpha $1.5 million CDN. Assuming the warrants are in the money, the various tranches from 2023 will most likely be executed once they near expiration date (or on a large share price spike) resulting in Alpha receiving capital. Let’s assume the $1.10’s are executed this year. This would result in $31.2 million CDN being deposited with Alpha.

This would lead one to believe that Alpha Lithium has plenty of capital to continue exploration of its properties, and given the share price they could raise additional capital if need be. Hence, Alpha passes the initial test of “Are they capable of funding exploration?” Any junior simply needs capital to continue exploring in order to prove up assets. Once proven, this often attracts joint ventures and/or buyouts. If it does not, then keep proving up assets till it does, as is often the name of the game in lithium.

The Basics of Alpha Lithium

Let’s glance at the projects for a minute and see if they make any sense. Simply having some cash in the bank does not correspond to having a good project. To borrow from my previous article on the property (and looking at any property) one needs to ask:

1. Are the lithium grades good? Obviously, this differs by resource type, be it brine-based lithium extraction (via water/evaporation), crushing lithium-laced rock, clay-based acid extraction or going with a DLE (direct lithium extraction) flavor.

2. Does the project have water?

3. Does the project have infrastructure? A project will need power. Projects need roads. Can failing equipment be brought to repair facilities for major repairs? If you are in the middle of nowhere, obviously operational costs will be high.

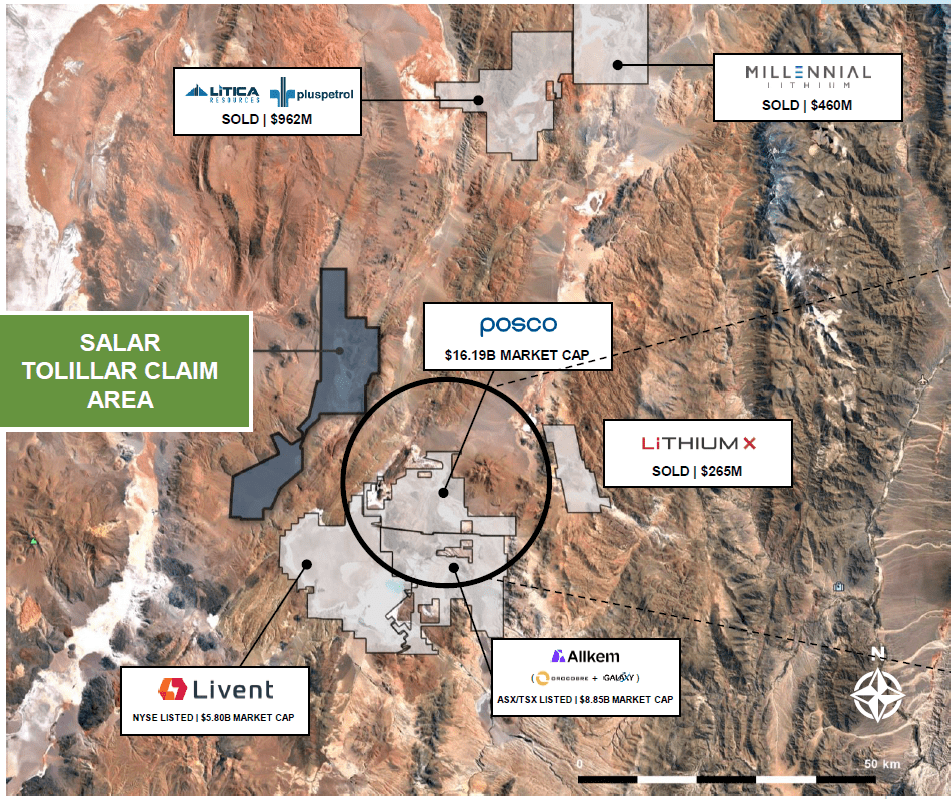

Given this criteria, let’s review. Alpha Lithium has two resources, with the most advanced being the Tolillar Salar resource in Argentina and the other being the quite famous Hombre Muerto basin.

We need to get a feel if we are looking at junk or if these are viable projects warranting more time and research. Looking at an overhead view on a map, Hombre Muerto appears to be in a good neighborhood with plenty of other projects nearby with infrastructure (roads, workforce, and power). Simultaneously, it appears that Alpha Lithium owns the entire Tolillar Salar.

Alphas Two Properties (Alpha Lithium )

Lithium Grades, Water, and Infrastructure

Given the proximity to other projects, attracting talent is possible. A gas pipeline and a road (unpaved) are 10km from the Tolillar property, while power is a bit farther out at 150 km north according to Alpha Lithium. At this point, they at least have my attention to scratch the surface a bit more. How are the lithium grades? Always assign caution when you see “up to” concerning a grade of lithium. What you need to confirm is the average grades. With the Tolillar Salar property, we see initial results from a mere 6 holes that range from 194mg/l to 345mg/l of lithium. Well enough for a DLE operation. Hombre Muerto lithium grades are projected to be in line with neighbors (aka high).

50,000 Tonnes

It was most interesting to see Alpha up the lithium carbonate plant estimated output in the Tolillar salar from 25,000 to 50,000 tonnes recently with an expected 40+ year mine life. An upcoming PEA (preliminary economic assessment) is in the works and an updated 43-101 “in the upcoming weeks”.

|

On a side note, it should be noted that Ausenco (the engineering firm that is conducting the PEA) is the same one that completed the study on Pozuelos /Pastos Grandes that PlusPetro (held via Lithea) was sold to Ganfeng (OTCPK:GNENY) for $950 million. This was mentioned by the CEO of Alpha, Brad Nichol. Was this an attempt to paint a similar future outcome in investors’ minds? Perhaps.

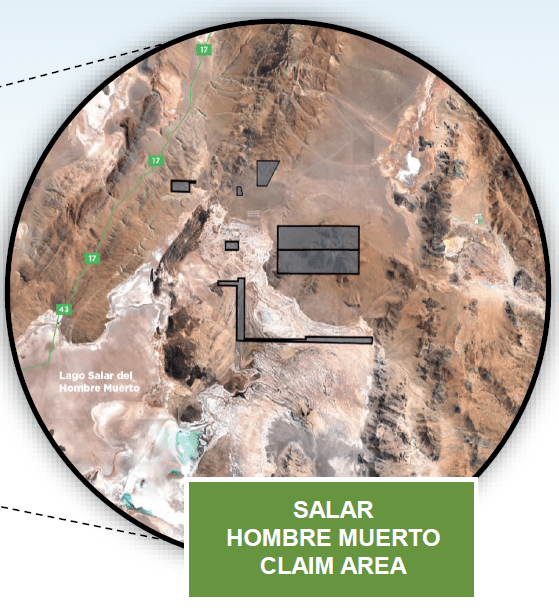

Hombre Muerto, All Drinking from the Same Lithium Well.

Alpha also acquired 5,000 hectares (12,325 acres) in the world-famous Hombre Muerto salar and as of January received rights to drill the land. An additional 5,700 hectares have been pre-awarded with contracts being finalized per the company. Given that some of the property is smack in the middle of POSCO/Livent area of operations, the odds of them hitting high grades like neighbors are very likely.

Alpha Lithium Property at Hombre Muerto (Alpha Lithium)

I highly doubt POSCO wants Alpha Lithium right in the middle of the area they are working in. If I were POSCO, I would be looking to acquire that property or perhaps if I were one of the larger producers, I would acquire it and then pump baby pump using DLE (direct lithium extraction).

Could Alpha bring this project to production? I think it is possible for a DLE project. On the other hand, you could simply drill it out, prove it up, and sell it off. If you sell it off that is one less straw sucking down the lithium in the basin because right now it is Livent (LTHM), POSCO (PKX), and Allkem (OTCPK:OROCF) all drinking from the same well.

Alpha Lithium is a Value Play

Back in Nov of 2021, a Russian outfit signed a potential deal with Alpha Lithium. For obvious reasons, this deal was never consummated given world events, but we can see the Russian valued Alpha Lithium much higher than it traded at the time (or even now). Per my last write up on Alpha:

While not exactly a NPV (Net Present Value), we can get a rough idea of the Tolillarprojects value. Per Alpha Lithium CEO Brad Nichol:

He now converts this from USD to CDN dollars:

|

As of 1/18/2023, the market cap is a mere $152 Million USD at a share price of $0.90. Compare that to the numbers above from the Russian deal and this might point to Alpha trading at a very favorable price. On an interesting note, the company’s book value is $0.39 a share due to the large cash position. What has changed since the canceled Russian deal is Alpha has acquired additional property and drilled out more of the property.

Alpha Lithium Risk

Alpha is non-revenue producing and has a burn rate. Lithium prices could come down and we might see sensational articles that say the sky is falling. I’m not seeing this yet, but it is only a matter of time if prices come down.

If lithium were to come down it would be a good thing in a sense. We want lithium to be affordable so the carmakers continue to embrace it. Alpha has a nice cash position that should last them roughly two years I would guess. Maybe more, but I’m just pondering all the drilling and exploration they are doing but back to risk. Alpha is a risky investment based in Argentina. Granted Argentina is a very favorable country for lithium investments, but it is still a foreign nation and that represents risk. Alpha is also a smaller company with limited resources. The point is if you are investing in Alpha Lithium you are taking an educated roll of the dice. During your investing journey things can and will go south. Plan on it and do not bet all of your chips on one bet. This is not to say you can’t bet hard, but never bet so hard that if you get deep-sixed and you are out of the game. Risk management is more important than potential gains. Always ask yourself “If I lose 100% of this bet and I’m lying in the “stock market intensive care unit” how do I look? Can I recover with time?”

Takeaway

Alpha is in my basket of lithium plays that I am invested in. I place high odds that the company will be acquired or take the project to production with a partner. Either way, this bodes well for investors with patience. Factor in resource expansions via additional drilling and a pending 5,700 hectares addition in Hombre Muerto and I think we have found our seeking alpha.